Reviewed by Tushar Sharma & Vaishali Sharma, Co-Founder, SafeRaho

Published 19 May 2026 · Updated 6 July 2026

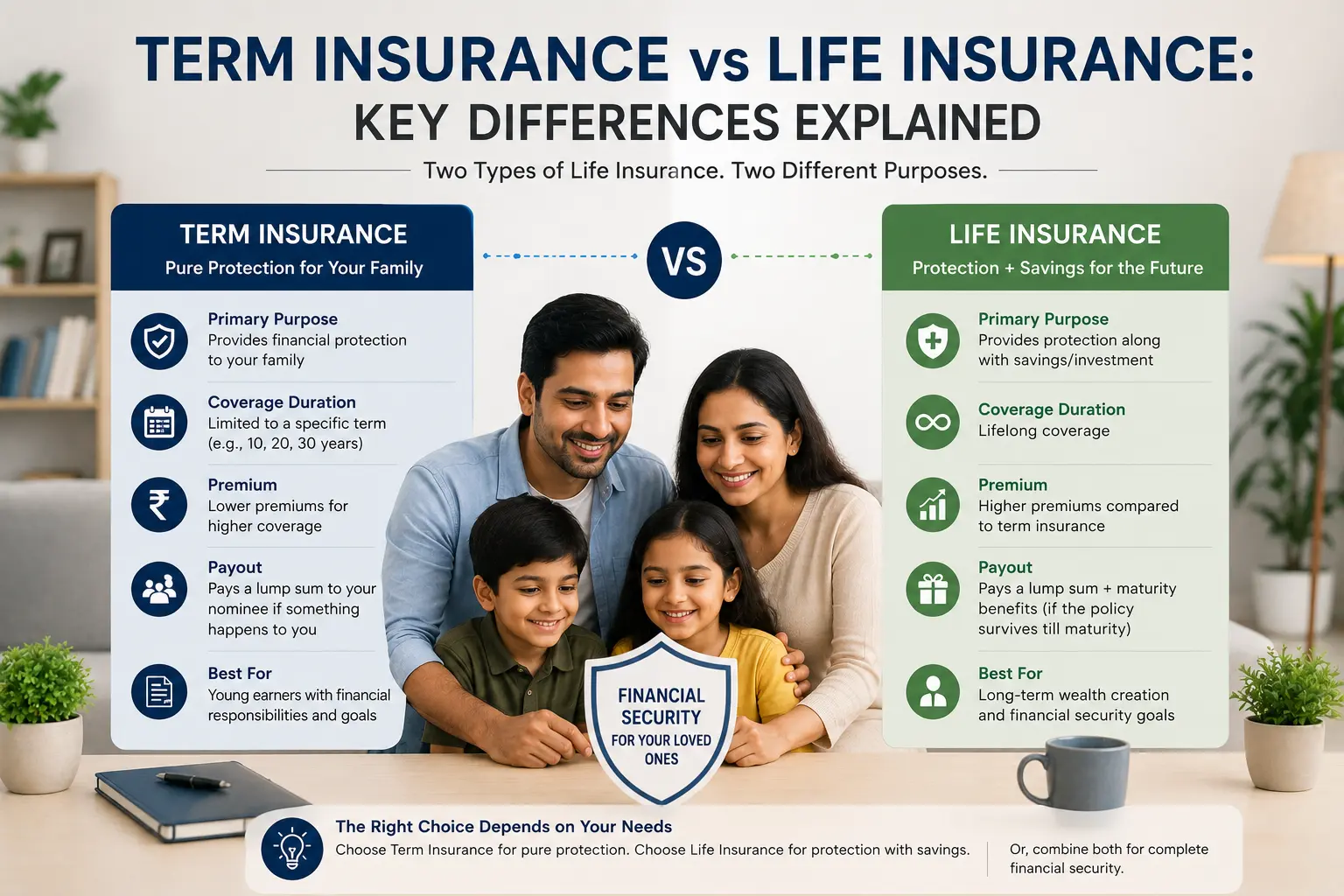

Term Insurance vs Life Insurance: Key Differences Explained

A lot of people compare term insurance and life insurance the same way people compare laptops at 2 AM after opening 47 tabs and emotionally deteriorating halfway through.

Everything starts sounding important. Everything sounds “guaranteed.” And somehow every plan claims to secure your family, your future, your retirement, and possibly the fabric of the universe itself.

So let’s simplify it.

If you're searching for term insurance vs life insurance, this guide explains the real differences in plain language.

What is Term Insurance?

Term insurance is pure financial protection.

You pay premiums for a specific duration.

If the insured person dies during the policy term:

- the nominee receives the payout

If the policyholder survives:

- there is usually no maturity benefit in standard plans

Simple.

Term insurance exists mainly to provide large life cover at affordable premiums.

What is Life Insurance?

“Life insurance” is a broad category.

In India, when people say life insurance, they often refer to traditional insurance plans that combine:

- insurance

- savings

- investment components

These may include:

- endowment plans

- money-back plans

- ULIPs

- whole life insurance

Unlike term plans, many life insurance policies provide:

- maturity benefits

- bonuses

- investment-linked returns

But they also usually cost significantly more.

Main Difference Between Term Insurance and Life Insurance

The biggest difference:

Term Insurance

Focuses mainly on:

- protection

Traditional Life Insurance

Combines:

- protection

- savings/investment

One is a shield.

The other is a shield carrying a suitcase full of financial products.

Term Insurance vs Life Insurance: Quick Comparison

| Feature | Term Insurance | Traditional Life Insurance |

|---|---|---|

| Purpose | Financial protection | Protection + savings |

| Premium | Lower | Higher |

| Coverage Amount | Higher | Lower |

| Maturity Benefit | Usually none | Usually available |

| Investment Component | No | Yes |

| Simplicity | Very simple | More complex |

| Best For | Income protection | Conservative savings |

Which One Gives Higher Coverage?

Term insurance usually gives much higher coverage for lower premiums.

Example:

| Plan Type | Annual Premium | Approx Coverage |

|---|---|---|

| Term Insurance | ₹12,000 | ₹1 crore |

| Traditional Life Insurance | ₹12,000 | Much lower coverage |

This is why many financial planners prefer term insurance for pure protection.

Why Term Insurance is Cheaper

Because it focuses only on risk coverage.

There’s:

- no maturity payout usually

- no savings component

- no investment returns

That simplicity reduces costs dramatically.

Think of it like ordering plain black coffee instead of a dessert beverage containing caramel galaxies and emotional support foam.

Why Traditional Life Insurance Costs More

Traditional life insurance plans often include:

- bonuses

- maturity payouts

- savings benefits

- investment elements

Part of your premium goes toward:

- insurance

- administrative costs

- investments

As a result:

- premiums increase

- life cover usually decreases compared to term plans

Who Should Buy Term Insurance?

Term insurance is generally ideal for:

- salaried professionals

- people with loans

- parents

- primary earners

- young professionals

- families needing high financial protection

Especially useful if:

- family depends on your income

Who May Prefer Traditional Life Insurance?

Some people prefer traditional life insurance because they want:

- guaranteed maturity value

- forced savings discipline

- conservative investment products

This can appeal to:

- risk-averse buyers

- people uncomfortable with market-linked investments

Though returns are often modest.

Very modest sometimes. Like “plant in a dark room trying its best” modest.

What Happens if You Survive the Policy Term?

Term Insurance

Usually:

- no payout

Unless it’s a Return of Premium plan.

Traditional Life Insurance

Usually provides:

- maturity benefit

- bonuses

- accumulated returns

Depending on policy type.

Which Option is Better for Young Professionals?

For many young earners:

- term insurance + separate investing

often provides better flexibility.

Why?

Because:

- term insurance gives large protection affordably

- investments can be managed separately

Instead of combining everything into one complicated product soup.

Term Insurance vs Whole Life Insurance

Term Insurance

Coverage for fixed duration.

Example:

- 30 years

- 40 years

Whole Life Insurance

Coverage may continue for entire lifetime.

Premiums are usually much higher.

Investment Returns Comparison

Traditional life insurance plans generally provide:

- stable

- conservative

- lower returns

Compared to market-linked investments.

Term insurance itself provides:

- no investment return

Its value comes from protection.

Common Mistakes People Make

Mixing Insurance and Investment Goals

Many people buy expensive policies without understanding:

- actual coverage

- returns

- fees

Buying Too Little Coverage

Some traditional plans offer very low life cover compared to premium paid.

Ignoring Inflation

₹10 lakh coverage may sound large today. Future reality may disagree aggressively.

Buying Based on Sales Pressure

Insurance should match:

- financial goals

- family needs

- income level

Not emotional sales presentations with dramatic background music.

Should You Buy Both?

In some cases: Yes.

Some people use:

- term insurance for protection

- separate investments for wealth building

Others may additionally choose:

- traditional plans for conservative savings goals

Depends on:

- risk tolerance

- financial strategy

- income

- goals

Important Things to Compare Before Buying

Always compare:

- Coverage amount

- Premium affordability

- Claim settlement reputation

- Policy flexibility

- Returns expectations

- Riders

- Long-term financial goals

Final Thoughts

The debate around term insurance vs life insurance becomes much simpler once you understand their actual jobs.

Term Insurance

Best for:

- maximum financial protection

- affordable premiums

Traditional Life Insurance

Best for:

- conservative savings

- bundled insurance + maturity benefits

For many modern families, term insurance acts like a financial safety net with laser focus.

No distractions. No decorative fireworks. Just protection when life decides to behave like an unexpected boss battle at level one.