Reviewed by Tushar Sharma & Vaishali Sharma, Co-Founder, SafeRaho

Published 18 May 2026 · Updated 12 July 2026

Section 80C Tax Benefits on Term Insurance Explained

Term insurance already protects your family financially.

Then the Income Tax Act walks in and says:

“Fine. You can save some tax too.”

That’s where term insurance tax benefits under Section 80C become useful.

If you're planning to buy a term plan in India, understanding these deductions can help reduce your taxable income while securing long-term financial protection.

And unlike many tax-saving products that arrive wrapped in complexity fog, term insurance tax benefits are actually fairly straightforward.

Mostly.

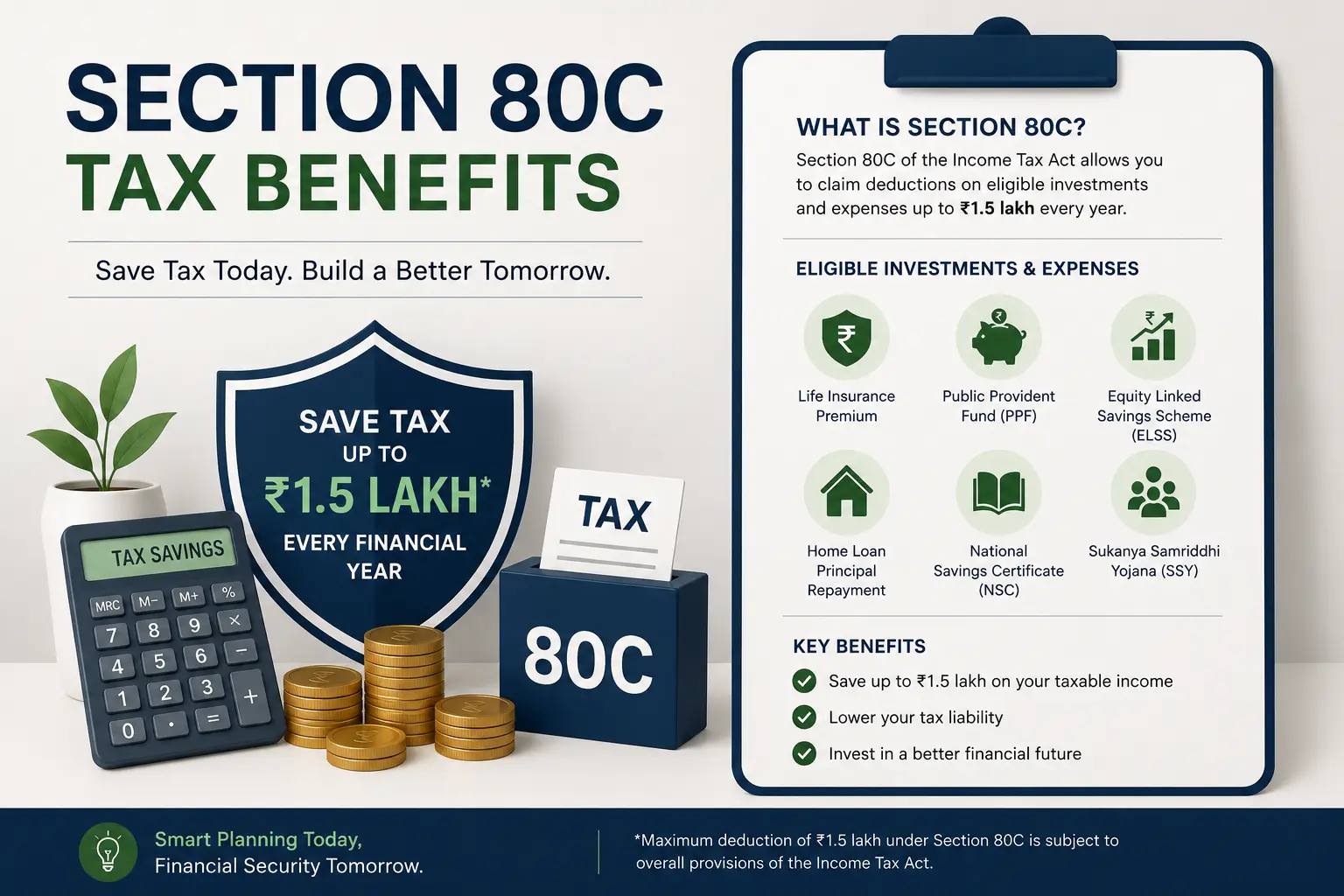

What is Section 80C?

Section 80C of the Income Tax Act allows individuals to claim deductions on eligible investments and expenses.

The maximum deduction allowed under Section 80C is:

₹1.5 lakh per financial year

This deduction helps reduce taxable income, and applies only if you're filing under the old tax regime (ClearTax: Section 80C).

Eligible investments under 80C include:

- PPF

- EPF

- ELSS

- Life insurance premiums

- Term insurance premiums

- Home loan principal repayment

Basically, Section 80C is the government’s annual:

“Please save responsibly” side quest.

Are Term Insurance Premiums Eligible for Tax Deduction?

Yes.

Premiums paid toward term insurance policies qualify for deduction under Section 80C.

This applies to:

- self

- spouse

- children

Whether dependent or independent.

Maximum Deduction Available

You can claim deductions up to:

₹1.5 lakh annually under Section 80C

This includes combined eligible investments and expenses.

Example:

| Investment Type | Amount |

|---|---|

| EPF | ₹60,000 |

| ELSS | ₹40,000 |

| Term insurance premium | ₹20,000 |

| Total Deduction | ₹1,20,000 |

Conditions for Claiming Section 80C Deduction

To claim the deduction:

- policy must be active

- premium must actually be paid

- premium should not exceed prescribed percentage of sum assured

Premium Limit Rule

For policies issued after April 1, 2012:

- annual premium should not exceed 10% of the sum assured (ClearTax: Section 10(10D))

Otherwise:

- deduction eligibility may get restricted to 10% of the sum assured, not the full premium paid

Example:

| Sum Assured | Maximum Eligible Premium |

|---|---|

| ₹1 crore | ₹10 lakh |

Though realistically, term insurance premiums are usually far lower than this.

If your premium somehow reaches ₹10 lakh annually, congratulations. Either your coverage is enormous or your insurer believes you wrestle volcanoes professionally.

Tax Benefits on Death Benefit

This is one of the biggest advantages.

Under Section 10(10D):

- death benefit received by the nominee is fully tax-free, with no upper limit on the premium or payout amount

This is different from the ₹5 lakh annual premium cap that applies to maturity payouts on non-ULIP policies issued after April 1, 2023 — that cap doesn't touch the death benefit, which stays tax-free regardless of how much premium was paid (ClearTax: Section 10(10D)). Since term insurance only pays out on death, not maturity, this distinction works entirely in its favour.

Meaning:

- family receives the full payout without any income tax liability

This makes term insurance highly tax-efficient.

Tax Benefits for Policies Bought for Family Members

You can claim deductions for premiums paid for:

- yourself

- spouse

- children

This applies even if:

- children are financially independent

However:

- premiums paid for parents are not eligible under your 80C deduction for life insurance

That part belongs to health insurance under Section 80D instead. Because Indian tax law enjoys creating alphabet sequels.

Old Tax Regime vs New Tax Regime

This matters a lot in 2026.

Old Tax Regime

Section 80C deductions are available.

You can claim:

- term insurance premium deductions

- other eligible deductions

New Tax Regime

Most deductions under Section 80C are not available under the new regime, which has been the default filing option since Budget 2023 (ClearTax: Section 80C).

Including:

- term insurance premium deduction

So your ability to claim tax benefits depends on which tax regime you choose.

Always compare total tax liability before deciding.

Example of Tax Savings

Example:

- Annual income: ₹12 lakh

- Term insurance premium: ₹25,000

- Other 80C investments: ₹1 lakh

Total deduction:

- ₹1.25 lakh

This reduces taxable income under the old regime.

Meaning:

- lower overall tax payable

Not life-changing billionaire energy. But still useful.

Should You Buy Term Insurance Only for Tax Saving?

No.

Tax benefit should be secondary.

The primary purpose of term insurance is:

- financial protection for dependents

Buying insurance only to save tax is like buying a fire extinguisher because it matches the curtains.

Why Term Insurance is Still One of the Best Tax-Saving Tools

Because it combines:

- high financial protection

- low premium cost

- tax deductions

- tax-free death benefit

Few financial products offer all four together so efficiently.

Common Mistakes People Make

Buying Tiny Coverage for Tax Saving

Some people buy:

- low coverage

- inadequate protection

just to claim deductions.

This defeats the entire purpose.

Ignoring Tax Regime Selection

Section 80C benefits work mainly under:

- old tax regime

Many people forget this.

Missing Premium Payments

Lapsed policies may affect tax benefits and coverage continuity.

Confusing Investment Returns with Insurance Protection

Term insurance is not designed for investment returns.

It is pure protection.

That simplicity is its strength.

Documents Needed for Tax Claims

Usually:

- premium payment receipt

- policy document

- insurer certificate if required

Keep records safely for tax filing.

Future-you will appreciate not having to search through ancient email ruins at midnight.

How to Buy Term Insurance Smartly

Before purchasing:

- compare insurers

- choose adequate coverage

- disclose medical history honestly

- review claim settlement reputation

- understand policy exclusions

And yes:

- tax benefits matter

But family protection matters more.

Final Thoughts

Understanding term insurance tax benefits under Section 80C helps you make smarter financial decisions while protecting your family’s future.

The biggest advantages include:

- deduction under Section 80C

- tax-free death benefit under Section 10(10D)

- affordable premiums for large coverage

A good term insurance plan is already valuable.

The tax deduction is basically the government tossing in a small cashback coupon for being financially responsible.